A small group of retail banks is capturing value at scale from generative and agentic AI while most of their peers remain stuck in isolated pilots. That is the central finding of a new BCG Executive Perspectives report, which identifies 10 capabilities these banks are investing in and quantifies the returns.

Today’s customers measure their bank against the AI-native experiences threaded through the rest of their lives: apps that answer before they finish asking, travel platforms that rebook a cancelled flight unprompted. Instant, contextual answers have become the expectation, and the gap widens every quarter a transformation roadmap slips.

BCG argues retail banks are structurally well placed to capture value from AI in retail banking, with high digitisation, rich data and customers already comfortable with GenAI tools. What separates the leaders in agentic AI banking, it says, is a few deep functional redesigns rather than effort scattered across micro use cases.

1. Customer intelligence and growth marketing

AI-first banks build synthetic customer personas from real behavioural data to test propositions before spending on media, and optimise for the generative search engines where BCG says 64% of buyers now research decisions.

Agentic systems run media buying and funnel experiments at volume, with one Latin American bank scaling to five times more experiments a month. The report puts the combined payoff at more than 40% higher sales of new-to-bank products and 40% lower acquisition costs.

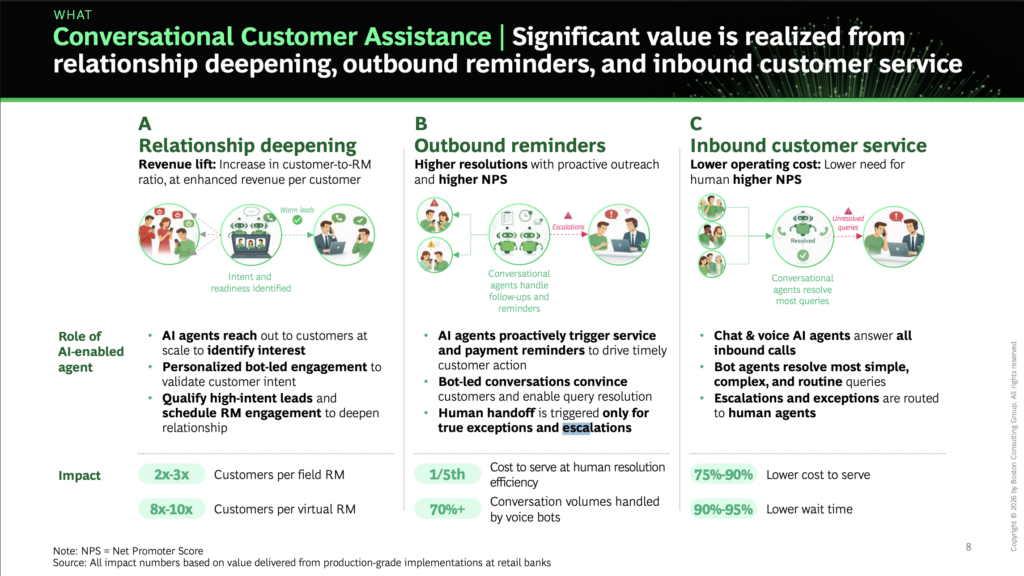

2. Conversational customer assistance

Agentic bots now handle engagement, inbound service, collections and reminders across voice and chat.

BCG reports that agentic voice bots manage more than 70% of human call volume at roughly a fifth of the cost, and argues banks should reconsider further investment in conventional call centres, reserving human agents for genuine exceptions and escalations.

3. An always-on relationship manager for every customer

This capability gives each customer a proactive AI agent that captures context from every interaction and responds with relevant offers. It runs on six coordinated layers: sensing, customer knowledge, decisioning, engagement, action and learning.

BCG cites a 60% rise in activation rates for new customers and a 20% to 40% improvement in cross-sell.

4. Banker productivity tools

Rather than replacing relationship managers, AI-first banks augment them with client-level agendas, personalised pitch books and process knowledge.

At Asian banks, BCG says, bankers using these tools engaged 50% of wealth clients weekly, up from about 15%, alongside a 20% rise in assets under management and conversions five to six times higher on select products.

5. Invisible operations

A “zero human operations” lane processes standard, and increasingly non-standard, files without manual touch, with agentic bots handling document recognition, extraction and fraud checks. Human experts step in only where routing rules require, while dynamic service-level agreements keep priority cases moving.

BCG reports 40% higher operational efficiency and 70% lower turnaround times.

6. A smart credit engine

Agentic underwriting compresses credit decision cycles by automating data extraction, risk assessment, income analysis and pricing, with human review retained in the loop.

Banks running these engines review 100% of submissions and quote five to 10 times faster, moving from weeks to days, according to the report.

7. Smart anti-financial-crime capabilities

Agent bots handle customer identification, screening, onboarding decisions and perpetual KYC monitoring, escalating only genuine high-risk cases to human reviewers. BCG cites cost savings of up to 50% at one European bank.

The pattern is already visible in Singapore, where Bank of Singapore has deployed agentic AI in KYC due diligence.

8. Smart collections

AI orchestration replaces granular segmentation models, using unstructured interaction data to understand why customers miss payments and to personalise outreach. Voice bots take more than 70% of collections calls, with offers based on a customer’s actual ability to pay.

BCG reports roughly 50% lower collections operating costs and a 10% to 20% reduction in net charge-offs.

9. Engineering, end-to-end

Beyond coding copilots, AI agents now run software delivery from AI-generated requirements through agent-native builds to autonomous release orchestration.

BCG puts the impact at 50% faster time to market, three times the engineering throughput and 70% less manual work.

10. The employee alter-ego

The final capability gives every employee a bot counterpart handling role-specific work, from credit-analyst agents to compliance monitors, and enabling tasks across HR, finance and IT.

BCG calls this early-stage, with at-scale impact still to come.

DBS Bank proves AI can deliver billion-dollar value

BCG’s thesis has at least one large-scale test case in the region. DBS generated about S$1 billion in economic value from AI, machine learning and data analytics initiatives in FY2025, up from S$750 million in 2024.

This is a figure built on roughly 370 AI use cases running on more than 1,500 models across the business. By early 2026, the bank had embedded generative and agentic AI across credit workflows, customer servicing, operations and cybersecurity.

This is a footprint that maps closely onto BCG’s smart credit engine, conversational assistance and invisible operations capabilities.

“We look at it from three lenses – personal agents, team agents and enterprise agents (which support complex agentic workflows),” Tan Su Shan, the CEO of DBS Bank, said.

The bank has been building its AI foundation for over a decade, which suggests the returns on offer are not a two-year transformation away for banks starting now.

The blueprint for scaling agentic AI

BCG is blunt about why value has stayed elusive elsewhere: banks chase isolated use cases, build solutions in search of problems, leave accountability ambiguous and treat risk as an afterthought.

Its remedy is to pick three or four transformation areas tied to strategy, embed value targets in operating plans, put the CEO visibly in charge, and design AI risk controls from day one.

Regulators are converging on the same point. The Monetary Authority of Singapore’s SAFR framework sets out safeguards for governing AI-agent actions in financial systems.

On the product-versus-platform question, the report lands on a pragmatic answer: start with a product approach focused on one business function, build every capability for reuse, and centralise GenAI technology early before federating as maturity grows.

For banks across Asia Pacific weighing where agentic AI investment goes next, BCG’s headline estimate is that 70% to 80% of routine toil and 30% to 50% of reasoning tasks can already shift to AI, leaving humans to focus where deep expertise matters.