India has turned its domestic payments app into an instrument of foreign policy. On 16 June 2026, Commerce and Industry Minister Piyush Goyal launched the Unified Payments Interface (UPI) at Galeries Lafayette in Nice, France, as reported by Business Standard, extending a real-time payments system built for Indian consumers into one of Europe’s busiest retail destinations.

The launch, India’s second in France after the past launch at the Eiffel Tower back in 2024, carries significant weight and a message. India’s payment rails are part of how the country delivers interoperable digital payment solutions across borders, with its benefits reaching beyond tourists.

The Domestic Scale Behind India’s UPI expansion

India’s UPI expansion abroad rests on a domestic base few payment systems can match. In January 2026, UPI processed 21.70 billion transactions worth INR 28.33 trillion (US$0.3 trillion), according to the Business Standard.

The International Monetary Fund named UPI the world’s largest real-time payment system by transaction volume, according to a note by the Ministry of Finance in India.

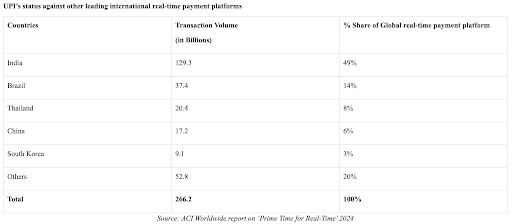

The note detailed that India’s UPI has ~49% share in global real-time payment platforms, even crossing Brazil, Thailand, and China.

The payment system has recently completed 10 years. As of March 2026, 703 banks are live on UPI, with eight countries accepting it: UAE, Singapore, France, Bhutan, Nepal, Sri Lanka, Mauritius, and Qatar.

The next decade for UPI involves bringing new users and merchants into its ecosystem, according to a recent press release by the Ministry of Finance. In order to make it work, efforts will be continued via technological advancements and policy support.

How India is Exporting the Technology Behind UPI

As of February 2026, India has signed cooperation agreements with more than 20 countries on its Digital Public Infrastructure (DPI), the open technology stack built under the India Stack initiative.

These are the same foundational layers that power UPI, alongside the Aadhaar identity system and the DigiLocker document wallet.

India is now sharing that technology with the world through programmes such as India Stack Global and the Global DPI Repository, positioning the country as a hub for digital public goods.

Governments across Africa, Asia and South America have already begun adopting the model, a measure of how far India’s DPI has travelled beyond its borders.

That momentum shows most clearly in UPI itself. The payments rail now runs live in more than eight countries, including the UAE, Singapore, Bhutan, Nepal, Sri Lanka, France, Mauritius and Qatar, with 30 or more additional markets reported to be in discussion.

Cross-border UPI transactions grew more than twenty times in the year to FY25, a trajectory which could have been tied to cheaper remittances, broader financial inclusion and a stronger Indian presence in global fintech.

UPI’s Southeast Asian Playbook Is Already Emerging

The clearest test case sits in a neighbouring country. India and Singapore linked UPI with PayNow in February 2023, in what the two regulators called the world’s first cloud-based, real-time cross-border payment linkage, launched jointly by the Monetary Authority of Singapore and the Reserve Bank of India.

At that point in time, the annual remittance flow between Singapore and India was said to be in the numbers of US$1 billion.

The groundwork ran deeper than the launch date suggests: the two sides had signed the underlying agreement back in September 2021, then spent eighteen months building the connection between NPCI International and Singapore’s payment operators.

The corridor is said to let users in both countries move money using only a mobile number or virtual payment address, with funds settling in seconds rather than the days a traditional remittance can take.

That speed attacks a real cost: cross-border transfers had typically run close to 5% of the sum sent, and the linkage was designed to cut that to less than half.

The link has since widened. National Payments Corporation of India (NPCI) International extended the service to 19 Indian banks on 17 July 2025, deepening a remittance corridor that leans heavily on the Indian diaspora in Singapore, including students and migrant workers sending money home.

The regional pattern is now spreading west. On 12 February 2026, the National Payments Corporation of India (NPCI) International signed an agreement with Payments Network Malaysia (PayNet) to connect UPI with DuitNow QR, Malaysia’s national QR standard, in phases.

In the first phase, Indian travellers will be able to pay at DuitNow QR merchants across Malaysia using their existing UPI-enabled apps. A later phase will let Malaysians scan UPI codes when visiting India, from which they would be able to pay via the e-wallet or banking app they opt to use.

For merchants, that opens millions of Malaysian acceptance points to Indian visitors, a prospect both sides have tied directly to the Visit Malaysia 2026 tourism push and the two-way travel it is expected to generate.

The Data Protection Question That is Unravelling

The export model carries an unresolved question about data. UPI does not sit on its own. It runs inside a wider stack that ties payments to Aadhaar identity records, which means the rails being exported move some of the most sensitive information a state can hold.

India’s safeguards are not static, and the recent direction cuts both ways. On the protective side, the central bank moved UPI to a risk-based authentication model from April 2026, letting platforms calibrate their security checks to each transaction’s risk profile rather than applying one uniform process.

The same reform shifted the burden of security away from individual users and onto banks and payment service providers, effectively treating UPI as national critical infrastructure, according to analysis by the Centre for Strategic and International Studies.

Where India’s UPI Expansion Goes Next

A payments app that began as a way to move rupees between bank accounts is now a lever of intelligence diplomacy and a test case for whether public digital infrastructure can scale across borders effectively.

The Nice launch will definitely not be the last. With agreements signed across the Global South and live corridors already running into Southeast Asia and the Gulf, the more interesting question is on whose terms the countries adopting it choose to run it.