Most Australian fintechs gaining ground in Southeast Asia got there by embedding inside local banks, not by competing with them for customers.

That partnership-first pattern, repeated across the sector’s biggest regional success stories, is the crucial finding of Austrade’s new industry capability report, which maps 896 active companies and treats the region as the prize.

The rankings and growth forecasts are in there too, but for fintech operators across ASEAN, the more useful question the report answers is a practical one.

Which Australian firms are coming, what do they sell, and how do they plan to land?

A mature fintech sector

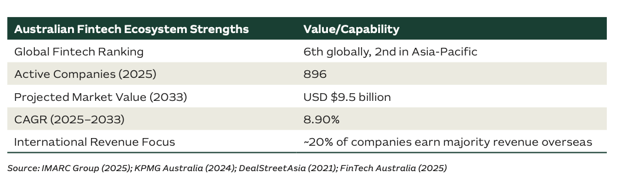

The report positions Australia as the world’s sixth-largest fintech market and second in the Asia Pacific, with its companies projected to push market value to US$9.5 billion by 2033, on an annual growth of about 8.9%.

Digital payments is the largest segment at roughly a fifth of companies, the same category that produced buy now, pay later (BNPL) pioneers Afterpay and Zip.

Lending, regtech, wealthtech, and blockchain and crypto follow. Sydney accounts for 59% of firms, with Melbourne and Brisbane making up most of the rest, a concentration the report links to tighter talent and knowledge clusters.

The sector has also consolidated. Active company counts moved from 830 in 2023 to 767 in 2024 before recovering to 896, which the report reads as a shift towards larger, more scalable businesses rather than a churn of early-stage startups.

Built to be exported

Around one in five Australian fintechs earn the majority of their revenue overseas, a figure the report treats as evidence that local solutions travel well. The analysis rests on a handful of capabilities, and regtech sits at the centre of it.

Australia’s compliance-heavy environment has produced firms that treat regulation as a product feature. This includes the Consumer Data Right open banking regime, which lets customers share their banking data with third parties, and a real-time payments system, which the report says processes more than two million payments a day.

That positioning is interesting for ASEAN markets that are building out their own frameworks. Compliance tooling, identity verification and automated reporting are the areas where regulators in Singapore, Malaysia, the Philippines and Indonesia are tightening expectations, and where established Australian vendors can plausibly claim a head start.

Three playbooks for Southeast Asia

The case studies are most useful for regional readers, as each shows a different route into the market.

Sydney-based identity verification firm Data Zoo leaned hardest on government support, using Austrade trade missions and Team Australia pavilions at the Singapore FinTech Festival between 2022 and 2024 to build credibility. This was before the firm raised A$35 million in 2024, its first outside funding after 13 years of bootstrapping.

Its pitch is compliance: international certifications and a privacy-first design built to satisfy varying data-residency rules across the region, with Singapore as the entry point and the Philippines as a second office.

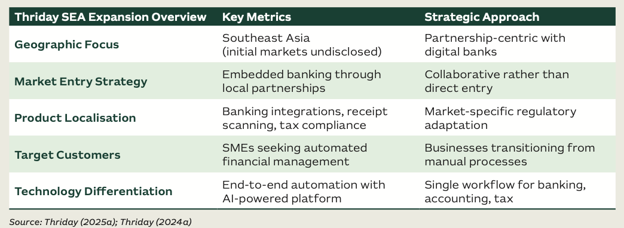

Melbourne’s Thriday, an all-in-one banking, accounting and tax platform for small businesses, took the embedded route, plugging its product into local digital banks rather than building its own distribution.

Embedding financial services inside a partner’s platform trades brand visibility for speed and for access to that partner’s existing customers and licences.

Sphere for Good, a climate fintech that calculates and offsets the carbon footprint of transactions, built its entry around a cornerstone partnership with Visa and local banks, starting in Vietnam, Malaysia and Singapore.

Its differentiator is mission rather than infrastructure, aimed at partners and customers who weigh sustainability metrics alongside financial ones.

The common thread is partnership over direct entry. Each firm uses a local bank, a card network or a government programme to shortcut the cost and time of going it alone.

The headwinds are real

Funding for Southeast Asian fintech fell about 75% from its 2022 peak to US$1.6 billion in 2024, and meaningful expansion now needs a capital commitment, the report puts at US$5 million to US$10 million per market.

Regional super apps Grab, GoTo and Sea control a large share of consumer financial services, which pushes smaller entrants towards business-to-business niches. Licensing can run 12 to 18 months and cost between US$500,000 and US$2 million per market.

Talent attrition reaches 30% to 40% in markets such as the Philippines, and cash still accounts for around 80% of transactions despite high mobile penetration.

hile none of these is critical, they favour patient, partnership-led players over those chasing rapid consumer scale.

Money is back, but pickier

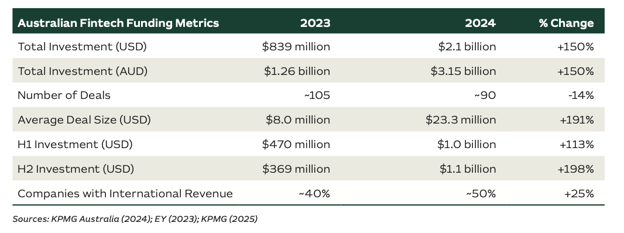

Australian fintech funding more than doubled to US$2.1 billion in 2024, though the recovery came from a handful of large deals rather than broad venture activity.

Deal volume actually fell 14%, and average seed rounds slid to about A$1.5 million, squeezing newer entrants out of the picture even as headline investment rose.

Regtech was the one subsector to attract more global investment, reaching US$7.4 billion in the first half of 2024, which the report attributes to demand for AI-powered compliance.

What it means for the region

Southeast Asia’s fintech opportunity for Australia is real but neither cheap nor fast, and the firms most likely to capture it are those willing to embed inside existing institutions rather than storm the market alone.

For ASEAN’s banks and digital lenders, that reframes Australian fintech in Southeast Asia as a source of partners more than rivals, offering compliance, payments and embedded-finance tooling in exchange for local reach and licences.

For regulators, a steady inflow of compliance-focused vendors is mostly welcome. And for the Australian sector itself, the report doubles as an argument that its next phase of growth depends on how well it plugs into the rest of the region.