The Monetary Authority of Singapore (MAS) and the Association of Banks in Singapore (ABS) have benchmarked PayNow against 11 of the world’s leading instant payment systems, and the exercise indicates where Singapore’s payment rail trails its peers, and where it leads.

Their PayNow Generation 2 Phase 1 report, published in June 2026, makes the case for turning a near-ubiquitous transfer service into a programmable, business-grade payments platform.

Here is what the PayNow Gen2 report found, what is driving it, and how the domestic payment rail could be transformed.

What the global benchmarking exposed

PayNow now reaches more than nine in ten adults and around 350,000 businesses. To find the gaps, MAS and ABS measured PayNow against 15 success factors across markets. The markets included Brazil, India, Malaysia, the UK and Hong Kong.

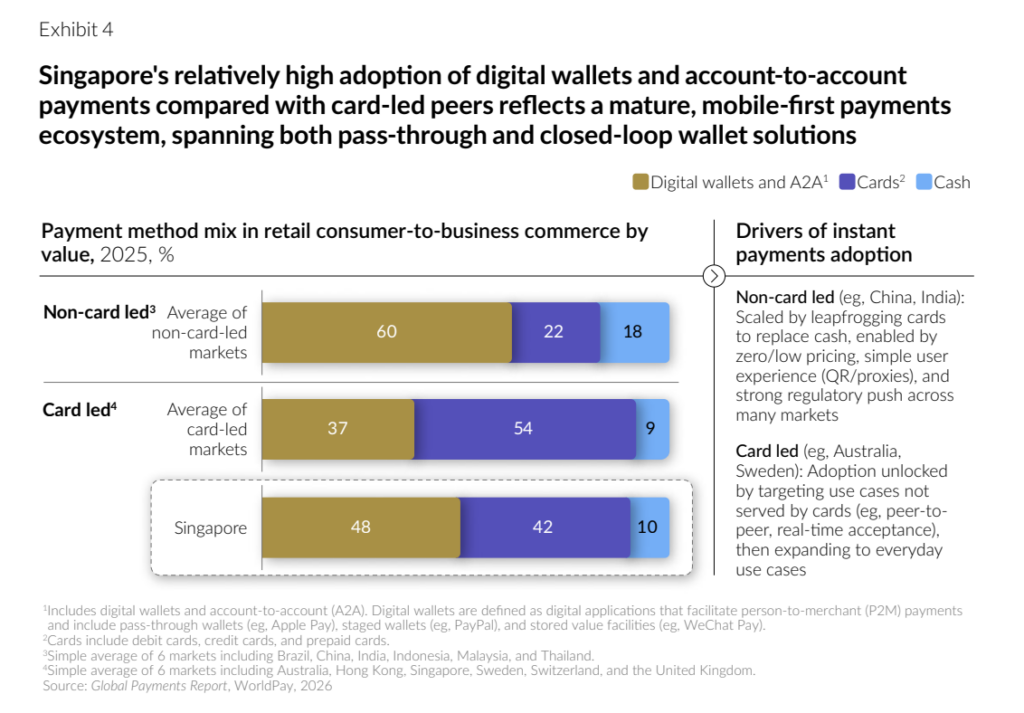

The rail scored well on the basics. It offers low-cost acceptance, roughly 25 to 80 basis points against the 250 to 300 charged by international cards, and it is free for consumers.

Its real-time, proxy-based design remains simple to use. Singapore also outperforms its card-led peers, with digital wallets and account-to-account (A2A) payments making up about 48% of retail consumer-to-business value, against a 37% average across comparable markets.

The report draws a useful distinction between two adoption playbooks. Brazil and India leapfrogged cards to replace cash, helped by near-zero pricing and QR-and-proxy simplicity.

Card-led markets such as Singapore instead won ground on use cases that cards served poorly, then expanded from there.

The shortfalls sit higher up the stack. PayNow lags on advanced consumer features such as recurring payments, request-to-pay and deep-linked checkout, capabilities that India’s UPI has made routine.

PayNow also supports a narrower set of business flows than the UK’s Faster Payments System, which clears values up to GBP 1 million and carries structured invoice data natively.

Its scheme-level plumbing, from dispute frameworks to structured data standards and release cadence, is also less mature than leading peers. Brazil’s Pix, for instance, ships coordinated upgrades on an annual cycle.

Five shifts redrawing the rules

The report sets its recommendations against five structural shifts reshaping payments worldwide.

The first is convenience: pay-by-chat and pay-by-voice flows, with artificial intelligence prefilling payee, amount and reference fields, are moving payments toward single-tap confirmation.

The second is agentic commerce, in which AI agents shop and pay under preset rules such as merchant whitelists and spending caps. The report treats this as a longer-term option for Singapore, contingent on clear rules over authorisation and where liability sits.

Third is programmable money. Stablecoin issuance has doubled since early 2024, with daily transaction values near US$30 billion, and regulatory clarity in markets including Hong Kong and the United States is lowering barriers to entry. In Brazil, some providers already let shoppers pay merchants via Pix using USD Coin, converted to local currency at checkout.

The fourth shift reframes trust as a product, as deepfakes and synthetic identities push networks to embed shared fraud controls and rapid account freezes by default.

Finally, the fifth embeds payments inside enterprise software, making structured, invoice-linked data the layer that lets accounting systems reconcile themselves.

Each shift carries a concrete implication for what a national rail must support.

Trust as a product points to network-wide detection of unusual activity and standard messages to freeze suspect accounts. The software shift points to invoice-linked request-to-pay, structured fields in settlement messages, and standardised exception codes.

These are the functions that PayNow’s redesign then tries to deliver.

The redesign: from transfers to a payments platform

One chapter in the report is dedicated to turning those pressures into four mutually reinforcing themes.

The first targets the consumer experience. Paying a merchant online today can mean saving a QR code, switching apps and returning to confirm. Deep-linking would collapse that into a single reviewed tap.

QR interoperability between PayNow and NETS would let any PayNow-enabled app pay at either scheme’s merchants, and MAS and ABS aim to pilot it by end-2026.

The second theme covers software-enabled business payments: preauthorised and recurring collections, structured data fields that carry invoice references for automated reconciliation, and a wider transaction range.

That range runs in both directions, from micropayments below S$1 to government collections above the current S$200,000 cap, each with its own controls.

The report is candid that pull-based payments shift control to the payee and need strong consent and dispute safeguards before any rollout.

The third theme broadens participation through indirect access for smaller payment service providers and foreign players, alongside deeper cross-border links to priority markets.

The fourth strengthens the scheme itself, spanning offline payments for continuity during outages, higher throughput, AI and machine-learning fraud management, standardised dispute resolution and recall-of-funds mechanisms, and a developer and application programming interface (API) ecosystem that lets third parties build on top.

MAS and ABS plan to sequence the work, prioritising customer experience, business payments and resilience in the near term, with cross-border expansion and programmable money set further out.

The report frames four near-term beneficiary groups: residents and tourists through QR interoperability, merchants through deep-linked checkout within a year, government agencies through a transaction-limit sandbox next year, and wider businesses through foundational work starting this year.

A delivery brief, not a product update

According to Gan Kim Yong, Deputy Prime Minister and MAS chairman, PayNow Generation 2 would be about “ensuring Singapore’s national payment schemes and rails are fit for purpose and ready for the future.

The near-term focus falls on smoother everyday payments, a larger role in business and government flows, and stronger scheme-level resilience, with richer data, micropayments and wider cross-border connectivity set further out.

Getting there depends largely on coordination. MAS keeps policy and regulatory oversight, covering safety, access, interoperability, competition and consumer protection, while ABS and other participants take on scheme governance and the build itself.

A Phase 2 study will develop and validate selected pilots, with an implementation roadmap due by the end of 2026.