Financial institutions increasingly view adverse media screening as part of their core financial crime defences, but many still depend on manual internet searches to carry it out.

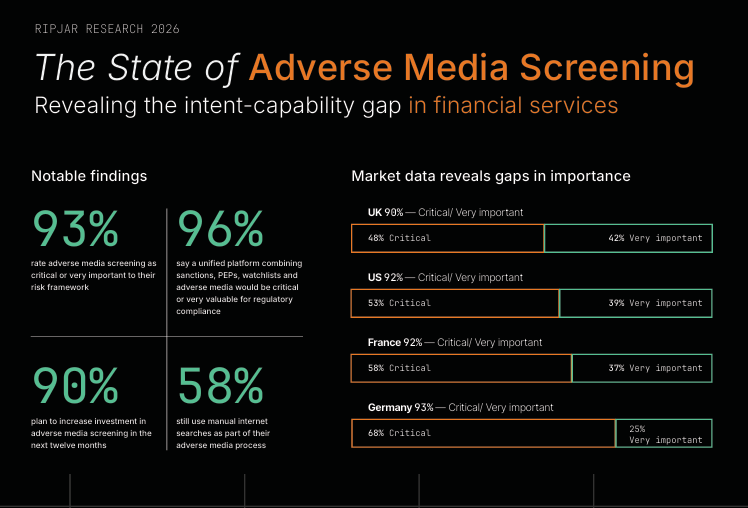

New research from Ripjar, a financial crime compliance technology company, shows 93% of financial services leaders rate adverse media screening as critical or very important to their risk frameworks. Yet only 77% currently conduct it, and 58% still use manual internet searches as part of the process.

The findings come from Ripjar’s 2026 State of Adverse Media Screening report, based on a survey of 400 senior financial services decision-makers across the UK, US, France and Germany.

Adverse media screening checks customers and counterparties against news and media sources for allegations of financial crime, fraud, corruption or other risks. It sits alongside sanctions, politically exposed person and watchlist screening within anti-money laundering programmes.

A manual process in a faster risk environment

The report points to a compliance function caught between rising expectations and uneven operating models.

Among firms that conduct adverse media screening, 81% use an integrated screening platform combining watchlists and adverse media, 74% use an automated vendor solution and 72% use real-time media feeds. But manual search remains firmly embedded in the process.

The US has the highest reliance on manual searches, at 70%. The UK follows at 61%, France at 59%, and Germany at 40%.

That regional gap is notable. Germany recorded the highest share of respondents describing adverse media screening as critically important, at 68%, and the lowest reliance on manual search. The UK had the lowest share rating it as critical, at 48%, while still recording higher manual use than Germany.

Ripjar suggests that manual search cannot provide the coverage depth, multilingual reach or diagnostic trail expected from modern screening programmes at scale. It also struggles to support continuous monitoring, where customer or counterparty risk profiles refresh as new information appears.

More than a quarter of firms surveyed, at 28%, do not yet run continuous, real-time monitoring. In those cases, adverse media risk may still depend on periodic checks or event-triggered reviews, leaving gaps between screening cycles.

Demand builds for unified screening

The survey shows a strong appetite for bringing different screening functions together.

Some 96% of respondents said a unified platform combining sanctions, PEPs, watchlists and adverse media would be critical or very valuable for regulatory compliance. The view was consistent across markets, reaching 95% in the UK, US and France, and 98% in Germany.

The numbers suggest financial institutions increasingly see these data sources as part of one risk picture rather than separate compliance exercises.

That matters because financial crime risk rarely appears neatly in one category. A customer may trigger concern through a combination of media allegations, sanctions exposure, political connections, corporate links or jurisdictional risk. Separate tools can leave teams reconciling alerts across different systems before they can understand the full profile.

Ripjar’s report frames this as an ‘intent-capability gap’: the distance between what compliance leaders believe adverse media screening should deliver and what their existing tools and processes can support.

AI plans remain ahead of deployment

Investment is coming into the market. Some 90% of firms surveyed plan to increase adverse media screening investment over the next 12 months, rising to 98% in the UK and 96% in the US.

Strategic AI adoption was the most commonly cited investment driver, at 79%, followed by regulatory focus at 77%, reputation risk at 74% and cost reduction and efficiency, also at 74%.

But AI use still trails ambition. While 79% cite AI as an investment driver, only 28% say they have fully deployed AI in screening operations. A further 44% have partially deployed it, while 22% remain at pilot stage.

For compliance teams, deployment depends on more than access to AI tools. Screening systems need clear source references, entity matching, decision histories and explainable outputs, particularly where alerts feed into regulated customer due diligence or escalation processes.

Matt Mills, chief executive officer at Ripjar, said financial institutions increasingly recognise the importance of adverse media screening, but approaches remain inconsistent.

“There’s a clear direction of travel in financial institutions when it comes to adverse media. With so many decision-makers viewing it as critical, adverse media screening is the first line of defence against crime and reputation risk,” he said.

“But what the research also reveals is that there are big differences across countries, and many are unprepared to run it in the way today’s market demands: systematically and at scale. Some of the best banks in the world are already doing this but it’s clear that the rest of the market needs to unify adverse media with sanctions, watchlists and PEPs screening if financial institutions are to adapt successfully to the new risk landscape.”

Enforcement risk sharpens the focus

The report links the screening gap to a tougher enforcement backdrop.

Financial institutions have paid more than $69 billion in anti-money laundering enforcement actions globally since the 2007 financial crisis. In 2024, penalties against banks worldwide rose 522% year-on-year to $3.65 billion.

Ripjar argues that adverse media signals often appear before enforcement action takes place. The challenge for financial institutions is whether they can surface relevant information early enough, assess it properly and act before regulatory or reputational damage lands.

The research was conducted by Vitreous World on behalf of Ripjar in April 2026. All respondents were C-suite or director-level decision-makers with responsibility for, or significant decision-making authority over, customer screening, anti-money laundering or financial crime activity.