The Asia Pacific data centre industry is experiencing a significant shift, from concentrated growth in traditional leading markets to rapid expansion in markets like Southeast Asia and India, according to CBRE’s 2026 Asia Pacific Data Centre Trends and Outlook.

Johor recorded the region’s fastest growth in live capacity, up 53% YoY, while Melbourne followed with expansion of more than 30%.

Power-Advantaged Markets Pull Ahead

Established hubs, including Greater Seoul, Sydney, Mumbai and Greater Tokyo, posted solid gains of 15% to 25% YoY, a notable result given the high base each carried into 2025.

Singapore and Hong Kong SAR grew more modestly, though the slowdown reflected development constraints rather than weak demand. In mainland China, growth eased as operators continued to fill existing vacant space.

The pattern points to demand consolidating in locations with reliable access to power at scale. Malaysia, Australia and India are capturing a growing share of new requirements as hyperscalers prioritise scalability and certainty of delivery.

Pipeline projects across these markets are now routinely sized in the hundreds of megawatts, with some campus developments approaching gigawatt scale.

A Broader and Deeper Demand Base

New demand is also emerging along the AI value chain. A growing cohort of neocloud operators is expanding quickly across the region to serve GPU-intensive training and inference workloads, adding diversity to a demand base long dominated by hyperscale cloud providers.

Government policy is reinforcing the trend. Australia’s National AI Plan and Korea’s “AI for All” scheme are among several national frameworks introduced across the region, designed to encourage investment, stimulate R&D and accelerate the rollout of AI-ready digital infrastructure. These programmes are expected to underpin demand over the long term while supporting the growth of local AI ecosystems.

Enterprise demand remains a steady foundation for colocation take-up. Corporations continue to upgrade their digital infrastructure, with financial institutions engaged in quantitative trading and major technology and manufacturing firms in the semiconductor and wider AI supply chain among the most active occupiers.

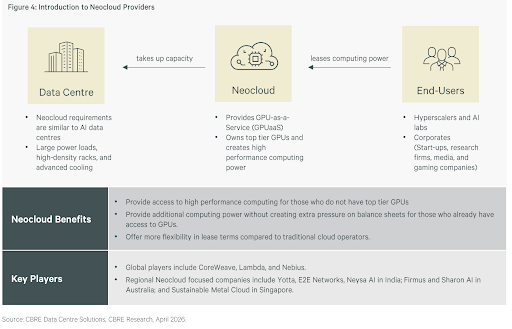

Neocloud Providers Emerge as a New Force

A defining theme of the past 12 months has been the rise of neocloud providers, a specialised category of cloud operator built for high-performance computing workloads.

Image credit: CBRE 2026 Asia Pacific Trends & Outlook

The sector first appeared in 2023 and 2024 and gained significant traction in 2025, with demand strong enough that some providers have already gone public.

Most large neocloud companies are currently based in the United States, but they are now pushing into Europe and the Asia Pacific. Within the region, AI demand and data sovereignty rules in certain markets are also encouraging local neocloud start-ups to take up data centre space.

These operators differ from established hyperscalers in important ways. Their operating track records are typically shorter and their credit profiles weaker, raising questions around tenant covenant strength.

Landlords, therefore, tend to favour operators with stronger financial backing, particularly where projects rely on debt financing, and lenders impose credit risk requirements.

Key regional neocloud-focused companies include Yotta, E2E Networks, Sustainable Metal Cloud in Singapore, and Neysa AI in India.

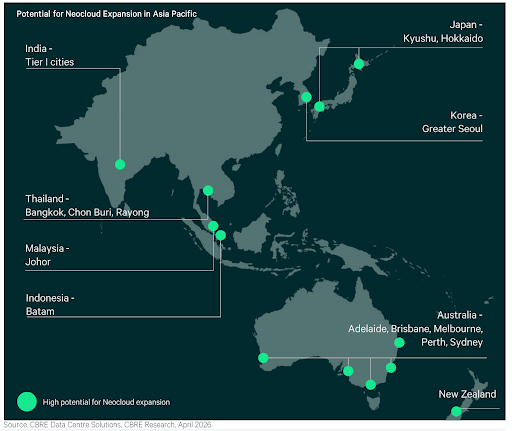

Growth Prospects Vary Widely Across the Region

The surge in near-term neocloud demand, especially for facilities able to support high-intensity workloads, has intensified capacity shortages within the Asia Pacific’s existing pipeline.

Opportunities differ across markets, largely according to power availability and infrastructure readiness.

North Asia offers limited headroom. Power constraints restrict development in core Tokyo and the Seoul area, Hong Kong SAR faces both inadequate power and unsuitable building specifications, and mainland China has sufficient power but limited access to GPUs. Pockets of opportunity remain, however.

Image credit: CBRE 2026 Asia Pacific Trends & Outlook

Kyushu and Hokkaido in Japan, along with upcoming projects in Greater Seoul, stand out for their stronger power availability and lower colocation pricing despite sitting outside core hubs.

South and Southeast Asia, excluding Singapore, hold considerable potential. Cheaper electricity, better access to power and permitting, and proximity to Singapore make Malaysia, Indonesia and Thailand attractive growth markets.

India is already familiar territory for the sector, with players such as Yotta and Neysa AI active, and rising high-performance computing demand is expected to drive further expansion.

Australia also presents strong prospects. With several hyperscalers already established, neocloud operators can help them scale, while abundant powered land supports development at a significant scale.

Construction Costs and Community Pushback Round Out the Obstacles

Beyond power availability, the main bottlenecks to data centre development in the Asia Pacific are largely the same as in previous years.

Elevated construction costs rank as the next most pressing concern, with fierce competition around AI buildout driving development costs significantly higher. Rising land prices, the adoption of advanced liquid cooling and compliance with sustainable building regulations all add to the bill.

Turner & Townsend’s Data Centre Cost Index 2025, the report indicated, ranked Tokyo as the region’s most expensive market to build in, with Singapore in second place. Kuala Lumpur has seen costs climb sharply on the back of spillover demand from Singapore.

India and mainland China remain comparatively cheaper, supported by lower labour and material costs, and some new developments in mainland China are using modular construction to shorten delivery timeframes.

Community resistance and long lead times for critical equipment present further hurdles, though experienced developers are becoming better at navigating both.

Yields Widen In Parallel With Interest Rate Increases

Data centre yields across Asia Pacific have diverged over the past six months, though movements have broadly tracked interest rates. In Australia and Japan, where rates rose during the period, yields expanded slightly to reflect the higher returns investors now require.

Greater China markets have seen yields hold largely steady, with activity dominated by platform deals and M&A.

Seoul and Singapore have reportedly experienced mild yield compression, as government backing for AI and a thin pipeline of large-scale capacity push investors towards existing stock, lifting price expectations.

Yield data for emerging Southeast Asia remains limited, given the scarcity of transactions, with most deals centred on land acquisition or development rather than stabilised assets.

Against this backdrop, investors are showing a clear preference for longer lease tenures with built-in rental escalation, seeking to preserve income certainty and cushion against interest rate risk.